Filter by

Promoting Enterprise blog (111)

RSS

Enrico Letta's report on the future of the Single Market will be out on 17 April!

Find out what's in this edition and access the full newsletter.

Discover the location and date of the SME Assembly 2024!

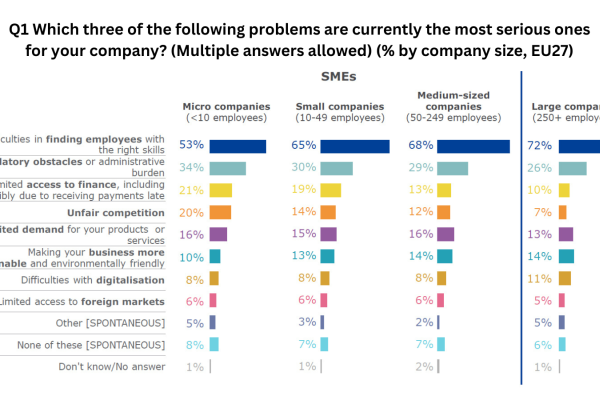

Having a workforce with the right skills contributes to sustainable growth, leads to innovation and improves companies' competitiveness. Take a look at some of the key recent findings of the Eurobarometer “SMEs and skills shortages”.

Read the comprehensive analysis of the trends in payment behaviour in commercial transactions in the EU to combat late payments

The 2024 European Enterprise Promotion Awards (EEPA) competition has officially launched! The EEPA has begun its annual search for Europe’s most successful promoters of enterprise and entrepreneurship.

Don't miss the final insights from this series about the EEPA winners! Read more about Greentech Procurement Accelerator.

Category 5, Supporting the Sustainable Transition winner ResC-EWE project answered to some of our questions, read more here.

Today let's meet the winner of the European Enterprise Promotion Awards, Category 4, Improving the Business Environment and Supporting the Internationalisation of Business.

"We showed that we can design and implement a project with various stakeholders over different geographies and connect people". Future Makers, winners of Category 1, Promoting the Entrepreneurial Spirit, comment like this their project.